Summary

Concerns over a blockade of the Middle East's Strait of Hormuz have collided with front-loaded ordering demand—shippers pulling volumes forward ahead of price increases—driving global shipping freight rates to their highest level this year. With both container and bulk rates rallying together, expectations are building for an earnings recovery across Korea's shipping industry, which has diversified its routes and vessel types. Because rate increases typically flow directly into shipping lines' operating profit, the short-term momentum is clear.

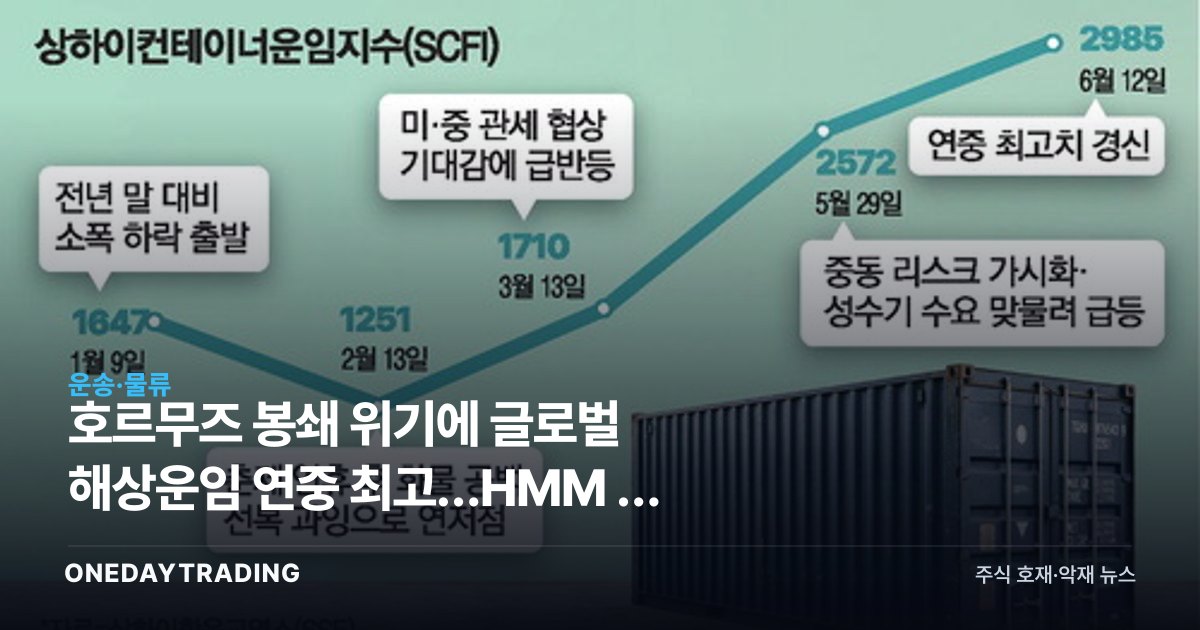

How It Unfolded

The primary trigger for this rate surge is geopolitical risk. The Strait of Hormuz is a critical chokepoint through which a substantial share of the world's seaborne crude oil traffic passes, and each time a potential blockade is floated, carriers review alternative routes, lengthening voyage distances and sailing days. That, in turn, shrinks available vessel capacity (supply) and pushes rates higher.

The second driver is demand-side front-loading. As cargo owners place orders earlier than usual out of concern over product price increases and supply chain disruptions, freight has concentrated on certain segments, sharply tightening short-term supply-demand (order flow). Layered on top is the structural impact of prolonged Red Sea and Suez detours, which has lifted the very floor of the rate curve.

Korean shipping lines have moved away from their past reliance on a single route and single vessel type, broadening their portfolios across containers, bulk, tankers, and gas carriers. Thanks to this structural improvement, analysts say they are now positioned to absorb the gains of a rising-rate phase relatively evenly, rather than being whipsawed by the volatility of any one route.

Structural Background

Shipping is a textbook cycle- and supply-sensitive industry. Because it takes several years from newbuild order to delivery, short-term supply is inelastic, so freight rates swing sharply whenever a demand shock or route disruption occurs. In recent years, tighter environmental regulations have increased the scrapping of older vessels and slow-steaming, further reducing effective capacity.

Geopolitical risk, in particular, effectively cuts supply by increasing distance. Carrying the same cargo over longer distances for longer periods reduces the number of voyages a given fleet can complete. Whether this rate strength is a mere temporary spike or an extension of a structurally high-rate phase will be the key variable for future earnings.

Stock and Sector Impact

- HMM: As the country's largest container carrier, it is the sector bellwether with the greatest operating profit leverage when the freight index rises. The effects of its route diversification and fleet expansion could come to the fore during a rate rally.

- Pan Ocean: With a high proportion of bulk carriers, this stock (ticker) is expected to benefit directly from rising raw-material cargo volumes and bulk freight rates.

- Korea Line: With a share of long-term shipping contracts and dedicated vessels, it offers a structure that can both defend against volatility and capture freight-rate upside.

- Refining and energy transport beneficiaries: When Hormuz risk is in focus, tanker rates and oil-price volatility rise together, rippling through related logistics cost structures.

- Export manufacturing burden: Conversely, a sharp gain (surge) in freight rates raises logistics costs, which can be a cost-pressure factor for some export manufacturers and distributors.

Bull vs. Bear Scenarios

The bull scenario is one in which Hormuz tensions drag on and front-loaded ordering demand persists into the peak season. If entrenched detour routes combine with a capacity shortage, the high-rate phase could extend on a quarterly basis, lifting both shipping stocks' earnings and share prices together. The bear scenario, by contrast, is one in which geopolitical tensions ease quickly and a demand vacuum emerges once the front-loaded orders are exhausted. In that case, rates risk retracing steeply and giving back the short-term gains. Ultimately, the durability of this rate strength depends on political and diplomatic variables and the pace of recovery in global consumer demand.

Investor Action Points

- Check weekly whether the trend in key freight indices such as the SCFI and BDI is holding, and distinguish a temporary spike from a structural rise.

- Use the flow of geopolitical news on Hormuz, the Red Sea, and similar areas—and whether detour routes become entrenched—as a leading indicator of earnings momentum.

- Because exposure differs by vessel type across containers, bulk, and tankers, review stocks (tickers) in a diversified way that matches the freight-rate phase.

- Bearing in mind that sharp gains (surges) in freight rates also bring high volatility, set scaled-entry and stop-loss rules in advance for any short-term overheating.

This article is content automatically summarized and analyzed based on an original news report. View original (Maeil Business Newspaper, Corporate)