Key Takeaways

The fight over data center permitting is shifting from a corporate convenience issue to a political risk that can slow the AI buildout at the state level. Pennsylvania's record $20 billion economic development deal, announced last June by Governor Josh Shapiro, has become a flashpoint between companies pushing to cut red tape and residents wary of the projects landing in their communities. For investors, the takeaway is that the bottleneck for AI infrastructure is increasingly land, power, and local consent, not just chips.

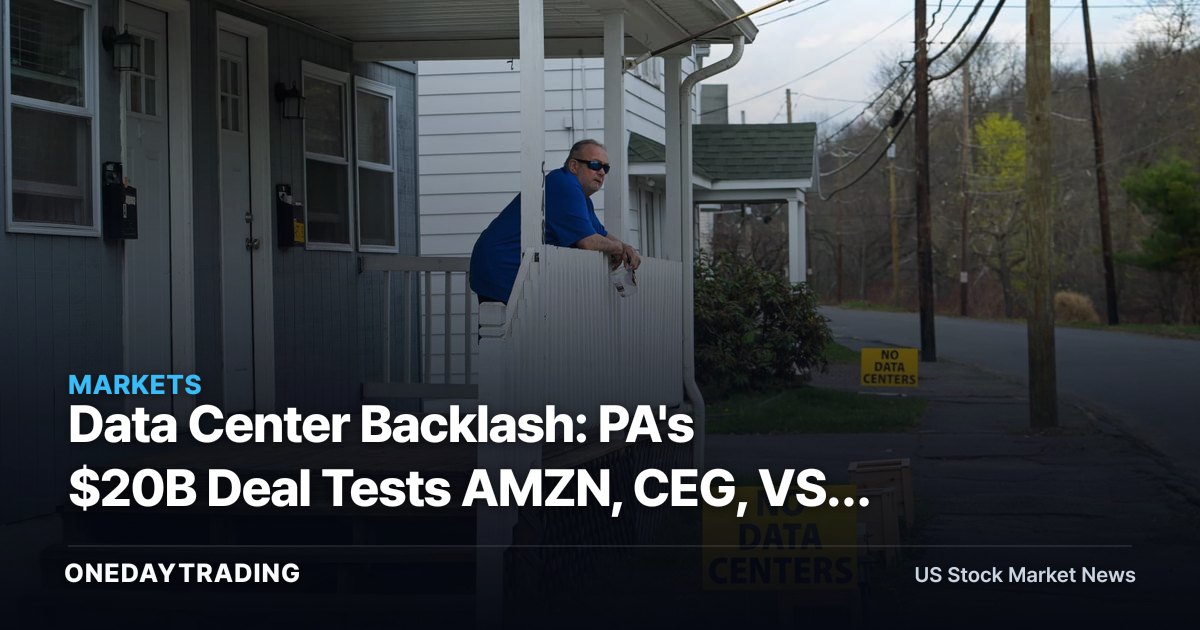

What Happened

Shapiro promoted the deal as the largest in state history, a marquee win for jobs and capital investment. Instead of a clean political victory, it has drawn sustained criticism, illustrating how data center growth collides with local concerns over land use, electricity prices, water, and noise.

The broader pattern is companies lobbying states to streamline approvals and speed construction, while a growing bloc of voters wants more scrutiny, not less. That tension matters because hyperscalers need predictable, fast permitting to hit aggressive capacity timelines, and any slippage pushes capacity online later and raises siting costs.

Background and Context

AI demand has turned electricity into the scarce input for compute. Each large campus can draw the equivalent of a small city, forcing operators toward states with available grid capacity and friendly policy. Pennsylvania, with its mix of nuclear and gas generation, is a natural magnet, which is exactly why a single $20 billion project carries outsized symbolic and economic weight.

Market and Stock Impact

- AMZN, MSFT, GOOGL: Hyperscalers are the buyers driving these deals; permitting friction lengthens lead times on capacity that underpins their cloud and AI revenue, pressuring return timelines on record capex.

- CEG, VST, TLN: Independent power producers benefit most directly, since data centers sign long-term contracts for firm power; local pushback that limits load growth or invites rate scrutiny is the key downside to that thesis.

- EQIX, DLR: Data center REITs monetize speed-to-power; slower approvals constrain new supply, which can support pricing for existing inventory but cap development pipelines.

- NVDA: Compute demand still flows through accelerators, but stranded or delayed power is the physical ceiling on how fast that silicon can be deployed.