Summary

As the U.S. and Iran implement their agreement to reopen the Strait of Hormuz shipping lane, tanker traffic has risen sharply over a short period. The key variable is the uncertainty over who will operate the strait once the toll-free transit period ends. This creates a direct path to profit-and-loss for Korean refiners, which rely heavily on Middle Eastern crude, and for airlines, where fuel accounts for a large share of costs.

The Full Story

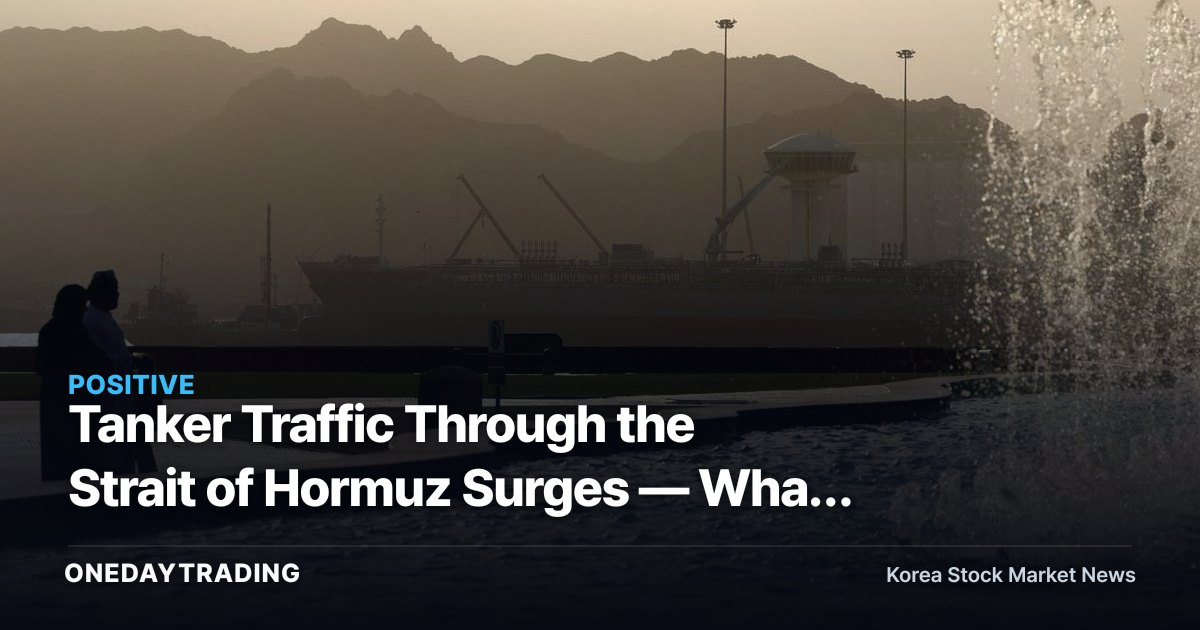

The Strait of Hormuz is a chokepoint through which roughly one-fifth of the world's seaborne crude passes, and it has been the spot that drives up the oil risk premium whenever military tensions escalate. With transit reopened under this U.S.–Iran agreement, tankers that had been waiting or detouring entered all at once, sending traffic surging.

The agreement reportedly includes a toll-free window during which no transit fees are charged for a set period. In the short term, this lowers shipping costs and normalizes supply flows, but with no decision yet on who will manage the strait and under what rules once the toll-free period ends, uncertainty remains over future transit costs and stability.

Korea depends on Middle Eastern producers such as Saudi Arabia, the United Arab Emirates, and Kuwait for a substantial portion of its crude imports, and most of that crude is shipped through the Strait of Hormuz. The stability of this chokepoint is therefore directly tied to the feedstock procurement costs of Korea's domestic refining industry.

Structural Background

When geopolitical tensions ease, the risk premium attached to oil tends to unwind, increasing downward pressure on international oil prices. For Korea, which imports all of its crude, stable oil prices act as a macro positive catalyst that simultaneously eases the trade balance, inflation, and corporate cost burdens. That said, the direction of oil prices is governed by a complex set of variables — not only the supply-side factor of normalized transit, but also global demand, producer output-cut policies, and exchange rates — so it is hard to call it one-directional.

Impact on Stocks and Industry Sectors

- S-Oil: It imports all of its crude and has Saudi Aramco as its parent, giving it the highest exposure to the Middle East and Hormuz among refiners. A stable shipping lane lowers the risk of feedstock procurement disruptions, but falling oil prices can lead to inventory valuation losses and refining-margin swings, making the impact double-edged.

- SK Innovation: With an integrated refining-and-chemicals business structure, it benefits from greater stability in crude supply, but product prices and refining margins (crack spreads) determine its actual earnings.

- Korean Air: Because fuel makes up a large share of operating costs, an easing of the oil risk premium is a direct beneficiary on the cost side.

- HMM: Normalized shipping lanes stabilize maritime transport flows, and falling oil prices create a path to lower bunker-fuel costs for its vessels.

- GS: It operates a refining business through its subsidiary GS Caltex and is affected by the stability of feedstock procurement.

Bull vs. Bear Scenarios

The bullish view is that normalized shipping lanes resolve supply jitters and lower the oil risk premium, which in turn translates into cost savings for airlines and logistics and stable operations for refiners. Conversely, the bearish view holds that if oil prices fall rapidly, refiners may incur valuation losses on their crude and product inventories and see refining margins squeezed, and that once the toll-free period ends and transit rules are renegotiated, freight rates and geopolitical uncertainty could resurface. Investors should note that for refining stocks, falling oil prices are not automatically a positive catalyst — earnings diverge depending on the margin structure.

Investor Action Points

- Confirm the end date of the Hormuz toll-free transit period and the terms of any subsequent agreement on operations and transit costs.

- Track Dubai and Brent crude prices alongside Singapore complex refining margins to gauge the real profitability direction of refining stocks.

- In refiners' next-quarter earnings, separate out inventory-related profit-and-loss from refining-margin items.

- For airline and shipping stocks, watch the oil-price level together with the won-dollar exchange rate to confirm whether fuel-cost savings are sustainable.

This article is content automatically summarized and analyzed based on the original news report. View Original (CNBC)